1. Purpose and object

1.1 The purpose of the Financial Regulations (hereinafter referred to as “the Regulations”) is to lay down the university’s principles of financial administration.

1.2 The Regulations lay down the basis for the preparation, approval, amendment, implementation of and reporting on the budgetary strategy and budget, the structure of the budget, the basis for taking financial obligations, the measures to be taken to ensure financial discipline, the terms and conditions for using the financial resources and the pricing principles.

2. Definitions

For the purposes of the Financial Regulations, the terms set out below have the following meaning:

2.1 “Sub-budget” means a subdivision specified in clause 5.3 of the university’s budget, for which a budget is prepared and approved, and the implementation of which is monitored and reports on which are prepared;

2.2 “Authorised signatory” means a person who has the right to sign expense receipts in sub-budgets and the constituent budgets. The authorised signatories are: the Rector, the head of the structural unit to which the financing source belongs; the university employee appointed by a written order of the Rector, area director or dean; the university employee appointed in a format which can be reproduced in writing by the head of the structural unit to which the financing source belongs;

2.3 “Budget” means an estimate of the university’s profit or loss, investment transactions, financing operations over the period of a financial year under accrual basis accounting. Cash flows recorded on cash accounting basis are purely informative;

2.4 “Financial year” means the period from 1 January to 31 December.

2.5 “Budgeting strategy” means a medium-term financial estimate based on the university’s strategic plan and objectives, which sets priorities by taking into account the existing financial resources.

2.6 “Budget surplus” means a situation where the operating revenue of the budget exceeds the operating expenses and the aggregate result is positive.

2.7 “Budget overrun” means a situation where the operating expenses of the budget exceed the operating revenue and the aggregate result is negative.

2.8 “Financing source” means the lowest level of the financial reporting structure in the accounting system, where revenues and expenditures, investment transactions, financing operations and cash flows on cash accounting basis are recorded and which may have its own budget if so decided by the head of the structural unit.

2.9 “Authorising officer” means a university employee, who gives orders for making purchases or covering expenses (excluding salaries) and making payments from the financing source either alone, if he or she is authorised to sign, or together with the authorised signatory, and who is required to prepare the budget of and report on the financing source and is responsible for the implementation and the balance of the budget and the balance of cash flow.

2.10 “Fund manager” means a person appointed by the Rector, who implements the budget of a structural unit instead of the head of the unit.

2.11 “Fund” means the financial resources intended to be used for a specified purpose or period, including contingency reserve for unforeseen expenditure.

2.12 “Spin-off company” means a research-based start-up company, i.e. a commercial undertaking, which uses the results or know-how of the university’s research and development in its activities.

2.13 “Department” means a structural unit at the department level, including colleges.

2.14 “Consolidated body” means a legal person in the university’s consolidation group.

2.15 “Office” means a structural unit subordinate to the area director appointed by the Rector’s directive.

2.16 “Project grant” means targeted funding received from other institutions, including private or public sector entities or international organisations (e.g. of the European Union), intended to cover the costs of an activity or set of interrelated activities with an established outcome, budget and defined time frame, for which no goods or services are directly received.

2.17 “Cash surplus” means a situation, where cash receipts exceed cash disbursements.

2.18 “Cash overrun” means a situation, where cash disbursements exceed cash receipts.

2.19 “School” means a school level structural unit, including the Estonian Maritime Academy.

2.20 “Activity support” means support, where the provider of the support does not impose strict restrictions on using the support and does not request distinction of expenditure covered from the support (incl. activity support for higher education, baseline funding of research and development institutions).

2.21 “Revenue sector” means teaching, research, business, support activities and general management.

2.22 “Fixed-term financing source” means a financing source, where the revenue, expenses, investment transactions, financing operations and cash flows (accounted using a cash accounting scheme) related to a project, service, grant, contract or any other funding that has a fixed term and goal and requires separate accounting is recognised.

2.23 “Permanent financing source” means a financing source, where the revenue, expenses, investment transactions, financing operations and cash flows (accounted using a cash accounting scheme) related to the main activity or services regularly provided by a structural unit are recognised.

2.24 “General funds” means the general teaching and research funds, the financing sources, where activity support, overhead allocations from the university’s revenue and other support and agreed allocations and their financial breakdown are recorded.

2.25 “Overhead allocation” means a financial allocation into the relevant general fund, which is determined based on the revenue and established by the Rector.

2.26 “University-wide project” means a university-wide development activity.

3. Principles of financial administration

3.1 The university’s financial administration shall be based on the budgetary strategy and the budget.

3.2 The university’s budget is balanced if the aggregate surplus/deficit equals zero.

3.3 The Rector has overall responsibility for preparing, implementing and reporting on the university’s budgetary strategy and budget.

3.4 The Finance Office shall arrange and coordinate preparation and approval of a budgetary strategy and budget in accordance with the Rector’s instructions and make sure that a report on the implementation of the budget is submitted and make proposals for imposing liability.

3.5 The heads of structural units and authorising officers shall report to the Finance Office.

3.6 The structure of the budget of a structural unit and a financing source shall be established by the Finance Office.

3.7 The heads of structural units shall be responsible for the preparation, the implementation, the balance of the budget and the balance of the cash flows of the structural unit.

3.8 The authorising officer shall be responsible for the implementation of the budget, the balance of the budget and the balance of the cash flows of the financing source.

3.9 The signatories and authorising officers shall avoid any conflict of interests, including transactions with respect to associated persons within the meaning of the Anti-corruption Act and shall act in compliance with the principles of avoiding a conflict of interests established at the university.

4. Budgetary strategy

4.1 A budgetary strategy shall be drawn up each year by budget sections and shall include an estimate of the next financial year and the following four financial years.

4.2 Information on revenue estimates for the coming years presented in the budgetary strategy of the previous year is amended upon approval of the new budget strategy only if the general objective of the revenue sector, the financial objectives of the university’s strategic plan, the economic forecast or the financial forecast change.

4.3 A budgetary strategy shall be accompanied by an explanatory memorandum.

4.4 A budgetary strategy shall be prepared for the university as a whole and does not include a breakdown by sub-budgets.

4.5 The Senate makes a proposal to the University Board for approving the budgetary strategy.

4.6 A budgetary strategy shall be submitted to the last meeting of the University Board held in the year.

5. Budget structure

5.1 A budget shall be divided into budget sections, which are broken down into sub-budgets.

5.2 The budget sections include:

5.2.1 the operating revenue budget;

5.2.2 the operating expenses budget;

5.2.3 the investments budget;

5.2.4 the financing operations budget;

5.3 The sub-budgets include:

5.3.1 the budgets of the schools;

5.3.2 the budget of the support structure;

5.3.3 the capital budget;

5.3.4 the budgets of funds;

5.3.5 the budgets of consolidated bodies.

5.4 A school sub-budget is broken down into the budgets of departments and dean’s offices.

5.5 The sub-budget of the support structure comprises the budgets of the Rector’s Office, University Board, Student Union, Offices and university-wide projects.

5.6 The capital budget comprises the budgets of property investments and repayment of capital and interests.

5.7 The sub-budgets of funds comprise the budgets of the funds laid down in the university’s budget.

5.8 The breakdown of revenue and expenses in the budget and the format of the budget is determined by the Chief Financial Officer.

6. Budgets of the schools and the support structure

6.1 Revenue is recognised in the budget of the structural unit, as a result of whose activities the revenue was received or who is entitled to receive the revenue pursuant to legislation.

6.2 Expenses are recognised in the budget of the structural unit, as a result of whose activities the expenses are incurred or who is obliged to incur the expenses, including overhead allocations into the general funds.

6.3 The structural unit that receives a grant shall pay the self-financing or co-financing required for the project grant from its budget revenue, including resources applied form funds, unless decided otherwise.

6.4 The structural units shall pay overhead allocation into the general fund at the rate and in compliance with the terms and conditions established by the Rector.

6.5 The terms of covering property management costs (costs of provision of premises), space allocation, the terms for using rental income and other related terms and conditions shall be set out in the rules for the use of the assets.

6.6 The structural units shall pay for the use of the premises in accordance with the rates established by the Rector and the rules for the use of the assets.

6.7 IT expenses shall be covered from the budget of the Information Technology Services. The budget for this purpose shall be allocated from the general fund and partly from the budgets of the structural units in accordance with the service charges established by the Rector.

6.8 Acquisition and depreciation of non-current assets, excluding acquisition and depreciation relating to real estate, is recognised in the budget of the structural unit that acquired or uses the non-current assets.

6.9 Ten per cent of the cost of each ECTS credit of degree studies declared by a continuing education student, excluding the ECTS credits of the Estonian Maritime Academy, Tartu College and Virumaa College, shall be included in the revenue of the Open University.

7. Capital budget

7.1 Investment property and loan servicing, including repayment of capital and interest, as well as the loans granted and received in compliance with subsection 8 (3) of the Tallinn University of Technology Act and secured obligations of other legal persons are recorded in the capital budget.

7.2 Investment property means purchase, construction of real estate property or major repairs increasing its value (included in the balance sheet).

7.3 In capital budgets, investments are broken down by property investment projects.

7.4 In order to finance a property investment, the Real Estate Development Director shall prepare the budget of the property investment, which shall include its total value and implementation by financial year. Financing will be started only if the corresponding budget has been prepared.

7.5 The sources for covering the capital budget are:

7.5.1 revenue or income from real estate transactions;

7.5.2 revenue from targeted support;

7.5.3 loans taken;

7.5.4 allocations from the general fund to the real estate fund.

7.6 Depreciation, amortisation and impairment losses related to real estate are recorded under expenses in the capital budget.

8. Budgets of funds

8.1 The volume of the Rector’s reserve fund shall be laid down in the budget and the Rector is in charge of the reserve funds.

8.2 Decisions on establishment and the financial volume of other funds are made during preparation of the budget and the general principles of the funds shall be described in the explanatory memorandum to the budget.

8.3 From the funds, allocations are made into sub-budgets or expenses are incurred based on the decision of the authorising officer of the fund for the purposes of fulfilling the goals of the university.

8.4 The budgets of the general funds are recognised in the sub-budget of the funds.

8.5 To allocate money from the budget of funds, excluding the Rector’s reserve fund and the real estate fund, the authorizing officer of the fund shall issue an order. The Finance Office shall make the corresponding change to the university budget based on the order.

8.6 Reporting related to the use of the fund’s resources shall be carried out in accordance with the rules laid down in the statute of the fund or established by the authorizing officer of the fund.

9. Budgets of consolidated bodies

9.1 A budget and an envisaged budgetary strategy of a consolidated body shall be submitted to Finance Office by the head of the institution by the date and on the terms and conditions established by the Finance Office.

9.2 A budget and an envisaged budgetary strategy of a consolidated body shall be submitted on the university’s budget form and it must be accompanied by an explanatory memorandum.

9.3 All transactions between the consolidated bodies and the university are eliminated in the university’s budget and the budget implementation report.

10. General funds revenue and its distribution principles

10.1 The general funds revenue and its distribution principles shall be set out in the university’s budget.

10.2 The sources of revenue of the general education fund include activity support, other institutional funding and allocations and overheads covered from the university’s revenue not allocated to the general research fund.

10.3 The sources of revenue of the general research fund include baseline funding and overhead allocations from the university’s research and development and business-related revenues. The doctoral allowance paid as part of the activity support and the salary grants of early stage researchers are also deemed to be revenue of the general research fund.

10.4 Funding from the general funds shall be allocated in the first place to:

10.4.1 the Rector’s reserve fund (the authorizing officer is the Rector);

10.4.2 the real estate fund (the authorizing officer is the Director for Administration).

10.5 Allocations from the general education fund shall be made as follows:

10.5.1 the baseline funding of the schools’ studies;

10.5.2 the teaching and learning development fund (the authorizing officer is the Vice-Rector for Academic Affairs);

10.5.3 partial funding of the university’s overheads;

10.5.4 targeted funding of the catering and seagoing practice of the students studying at Estonian Maritime Academy according to the study programmes governed by the Maritime Safety Act allocated based on the established rates;

10.5.5 targeted funding of the professorships established on the basis of subsection 9 (3) of the Tallinn University of Technology Act.

10.6 Allocations from the general research fund shall be made as follows:

10.6.1 the core funding of the schools’ research;

10.6.2 the grant fund (the authorizing officer is the Vice-Rector for Research);

10.6.3 partial funding of the university’s overheads;

10.6.4 targeted funding of doctoral allowances and early stage researchers’ salary.

10.7 The following shall be covered from the general funds:

10.7.1 organisation of studies, overall process and capacity of research and development activities and functioning of the schools, including overheads of premises and payment of remunerations of professors emeriti and doctoral allowances and doctoral students’ salary;

10.7.2 development of study programmes;

10.7.3 sustainable development of academic units;

10.7.4 the overall functioning of the university, the sustainable development of administrative and support structures, the university’s overheads.

10.8 The following shall be covered from the core funding of the schools: the costs of tenured positions and other permanent academic positions, teaching, organisation of studies, research and development, business cooperation and support activities related to serving society, development and other expenses of study programmes, management costs of the schools and departments, costs of the support structure of dean’s offices and other general expenses.

10.9 The core funding allocations of schools are made as a block grant. The amounts calculated by the apportionment formulae are not allocated for specific purposes and are distributed in compliance with the decisions made by the persons and councils responsible for the budget.

10.10 First, the funding of the teaching and development fund shall be allocated from the schools’ general education fund.

10.11 From the general education fund 50,000 euros is allocated annually for each professor post established based on subsection 9 (3) of the Tallinn University of Technology Act, which has been filled as of the beginning of each financial year, and the amount is transferred to a separate financing source created for and at the disposal of the respective post.

10.12 From the general education fund, targeted funding of the catering and seagoing practice of the students studying at Estonian Maritime Academy according to the study programmes governed by the Maritime Safety Act is allocated based on the established rates.

10.13 From the core funding of a school, 50,000 euros is allocated annually for each tenured post filled as of the beginning of each financial year, except for professor posts established based on subsection 9 (3) of the Tallinn University of Technology Act, and the amount is transferred to a separate financing source created for and at the disposal of the respective tenured professor post.

10.14 From the core funding of the schools, 70% shall be allocated for baseline funding and 30% for performance-based funding.

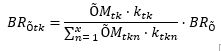

10.15 The baseline funding for teaching of the schools is distributed between the schools in accordance with the their share obtained using the following formula:  ,whereas the abbreviations in the formula stand for:

,whereas the abbreviations in the formula stand for:

10.15.1 baseline funding for teaching – BRÕ

10.15.2 the school’s baseline funding for teaching – BRÕtk

10.15.3 The arithmetic average workload of teaching at the school in the last three academic years, the workload calculated in accordance with the rules for calculating the workload of teaching of academic structural units – ÕMtk

10.15.4 The school’s equalization coefficient – ÕMtk

10.15.5 number of schools to whom baseline funding is allocated – x;

10.15.6 index of the concrete school – n;

10.16 The school’s equalization coefficient is the ratio applied to workload for the purpose of equalising transition from the previously valid core funding model of the schools to the new model.

10.17 The values of the schools’ ktk equalization coefficients from 01.01.2024 to 31.12.2025 are as follows: [entry into force 01.01.2024]

10.17.1 the School of Business and Governance 1.000;

10.17.2 the School of Information Technologies 1.045;

10.17.3 the School of Engineering 1.157;

10.17.4 the Estonian Maritime Academy 1.410;

10.17.5 the School of Science 1.474.

10.18 The proportion of performance-based funding of studies shall be calculated based on the following performance indicators of the school:

10.18.1 the share of students who graduate within the nominal period of study: weight 60%;

10.18.2 the share of master’s study programmes where at least 75% of the contact hours are taught by academic staff with a PhD degree or equivalent qualification, weight 20%;

10.18.3 revenue from continuing education: weight 20%;

10.19 First, the funding of the grant fund shall be allocated from the schools’ general research fund.

10.20 Targeted funding of doctoral allowances and early stage researchers’ salary is allocated from the general research fund.

10.21 From the core research funding of the schools, 60% shall be allocated for baseline funding and 40% for performance-based funding.

10.22 The baseline funding for research of the schools shall be distributed between the schools according to the methodology laid down in the Regulation of the Minister of Education and Research “Conditions and Procedure for Baseline Funding of Research and Development Institutions”. As an exception, from among the publications taken into account upon calculating baseline funding, only the articles published in journals belonging to the first and second quartiles of the SCOPUS SciVal and Web of Science databases are taken into account. The coefficients applied to publication shall not be used in baseline funding. For the purpose of the general research and development fund, the proportion of the funding of the schools is calculated on the basis of the average result of the last three years. The share of the school’s baseline funding is calculated based on the average result of the last three years. In order to find the amount of the school’s baseline funding for research, the share of the school’s baseline funding is multiplied by the total amount of baseline funding for research.

10.23 The proportion of performance-based research funding shall be calculated based on the following performance indicators of the school:

10.23.1 high-level publications, weight 30%;

10.23.2 the effectiveness of doctoral studies, weight 40%;

10.23.3 the performance-based funding of entrepreneurship, weight 30%.

10.24 A school’s share of core funding from the two general funds in total shall not decrease by more than 5% in a calendar year and is equalized by reducing the core funding of other schools proportionally according to their calculated shares prior to equalization.

10.25 The principles of financing a school and its structural units from the general funds:

10.25.1 the funding of a school is calculated by the structural units of the school;

10.25.2 the funding not directly related to a structural unit of the school (e.g. per cent of graduation within the nominal duration of study, etc.) is recognised on the budget line of 10.25.3 the dean’s office of the school;

10.25.4 the Finance Office shall submit the data on funding of schools and their structural units from the general fund to the dean;

10.25.5 in order to achieve the goals listed in clause 10.7, the dean shall allocate sufficient resources from the baseline and performance-based funding to academic structural units, taking into account the development goals of the school and its structural units, the number of tenured posts, the study load, the results of the structural units, etc.

10.26 The following shall be covered from the overheads of the university:

10.26.1 expenses of the support structure of the university, including the personnel expenses of the structural units in accordance with the composition of the staff and salary rate and other operating expenses, including the expenses of the premises used or possessed directly by the support structure in compliance with the rules for the use of the assets;

10.26.2 costs of development projects on the basis of an application of the area director;

10.27 Resources from general funds shall be allocated to the capital budget with the aim of keeping the aggregate result of the capital budget neutral throughout the financial year in order to enable sustainable development of the university’s real estate.

10.28 The Rector’s reserve fund shall be set up on account of the university’s general funds and it forms 2.5% of the volume of the general funds.

10.29 Allocations for covering the university’s overheads are made based on expenditure estimates.

10.30 In order to account for performance-based funding and shape the university’s budget, the following shall be submitted to the Finance Office: the underlying data of the calendar year preceding submission of the data regarding the performance indicators 10.18.3, 10.23.1, 10.23.2, 10.23.3 as of 30 December, the underlying data of the previous academic year regarding the performance indicators 10.18.1, 10.18.2 as of 15 August and data on baseline funding for teaching and the latest available data on baseline funding for research during the 34th week of the current year, whereas:

10.30.1 the Office of Academic Affairs shall submit data regarding the baseline funding for teaching and the performance indicator 10.18.2 by department;

10.30.2 the Office of Academic Affairs shall submit data regarding the performance indicator 10.18.1 by school;

10.30.3 the Finance Office shall submit data regarding the performance indicators 10.18.3 and 10.23.3 by department, while the Technology Transfer Office shall submit the underlying data regarding the performance indicator 10.23.3 at the contract level;

10.30.4 the Research Administration Office shall submit data regarding the baseline funding for research and the performance indicators 10.23.1 and 10.23.2 by department;

10.30.5 the Real Estate Development Director shall submit data on the area of the premises used by the structural units and the estimated premise expenses in the following financial year. The estimates shall be provided by structural unit (including by department and office) by indicating the expenses incurred by the structural units by direct use of the premises and proportionally with regard to premises to be taken into use.

10.30.6 The providers of underlying data shall be responsible for the accuracy of data submitted and for submission of the data by the due date.

10.31 Rules for the calculation of the performance indicator 10.18.1: percentage of students who graduate within the nominal period of study:

10.31.1 the performance indicator is one of the key performance indicators described in the university’s Strategic Plan 2021-2025;

10.31.2 for each school, the individual target for the academic year approved in the school’s action plan is taken into account;

10.31.3 if the implementation rate of an individual target is 100%, the school’s share of the performance indicator in the baseline funding formula of teaching is multiplied by the amount of funding of the performance indicator;

10.31.4 per each 1 percentage point by which the target is exceeded, the financial volume of the performance indicator increases by 4% compared to the 100% implementation rate (and linearly at intermediate points);

10.31.5 per each 1 percentage point by which the school falls short of the target, the financial volume of the performance indicator decreases by 6% compared to the 100% implementation rate (and linearly at intermediate points);

10.31.6 the financial deficit or surplus of the given performance indicator is equalized by the budgeted volume of the teaching and learning development fund.

10.31.7 The performance-based funding is obtained according to the following formula.

where the abbreviations in the formula stand for:

10.31.7.1 the school’s performance-based funding based on the percentage of students who graduate within the nominal period of study TRÕtk-;

10.31.7.2 the value of the performance indicator: percentage of students who graduate the school within the nominal period of study TÕtk;

10.31.7.3 the school’s target for the percentage of students who graduate within the nominal period of study TÕEtk;

10.31.7.4 The arithmetic average workload of teaching at the school in the last three academic years in accordance with the rules for calculating the workload of teaching of academic structural units ÕMtk;

10.31.7.5 the school’s equalization coefficient ktk;

10.31.7.6 the total amount of performance-based funding for the percentage of students who graduate within the nominal period of study TRÕ.

10.32 Rules for calculating the performance-based indicator 10.18.2: at least 75% of the volume of the master’s programmes is taught by academic staff members with a PhD or an equivalent qualification:

10.32.1 the performance indicator is one of the key performance indicators described in the university’s Strategic Plan 2021-2025;

10.32.2 for each school, the individual target for the academic year approved in the school’s action plan is taken into account;

10.32.3 if the implementation rate of an individual target is 100%, the school’s share of the performance indicator in the baseline funding formula of teaching is multiplied by the amount of funding of the performance indicator;

10.32.4 if the school falls short of the individual target, the100% implementation rate is multiplied by the actual implementation rate of the target;

10.32.5 no additional funding will be allocated if the individual target is exceeded. The financial surplus of the given performance indicator is transferred to the teaching and learning development fund.

10.32.6 The performance-based funding is obtained according to the following formula.

where the abbreviations in the formula stand for:

10.32.6.1 performance-based funding for the performance indicator: at least 75% of the volume of the master’s programmes is taught by academic staff members with a PhD or an equivalent qualification TR75%tk;

10.32.6.2 value of the school’s performance indicator: at least 75% of the volume of the master’s programmes is taught by academic staff members with a PhD or an equivalent qualification T75%tk;

10.32.6.3 the performance target for the school’s performance indicator: at least 75% of the volume of the master’s programmes is taught by academic staff members with a PhD or an equivalent qualification TR75%Etk;

10.32.6.4 the arithmetic average workload of teaching at the school in the last three academic years in accordance with the rules for calculating the workload of teaching of academic structural units ÕMtk;

10.32.6.5 the school’s equalization coefficient ktk;

10.32.6.6 total amount of performance-based funding for the performance indicator: at least 75% of the volume of the master’s programmes is taught by academic staff members with a PhD or an equivalent qualification TR75%.

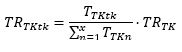

10.33 Rules for calculating the performance indicator 10.18.3: revenue from continuing education:

10.33.1 Revenue from continuing education includes the revenue recognised in the report on the implementation of the university’s budget as revenue from Open University tuition fees and sales of continuing education courses.

10.33.2 The performance indicator of each school is calculated based on the school’s share of the volume of the revenue from the continuing education of all the schools multiplied by the total amount of the performance indicator.

10.33.3 The performance-based funding is obtained according to the following formula.

where the abbreviations in the formula stand for:

10.33.3.1 performance-based funding of the school based on the revenue from continuing education TRTKtk;

10.33.3.2 value of the school’s performance indicator TTKtk;

10.33.3.3 number of schools – x;

10.33.3.4 index of the concrete school n;

10.33.3.5 the total amount of performance-based funding for continuing education TRTK.

10.34 Rules for calculating the performance indicator 10.23.1: high-level publications:

10.34.1 The performance indicator is calculated based on the number of papers per an academic staff member with a PhD published in journals ranked in the first quartile (Q1) according to SNIP scores calculated from SCOPUS SciVal data (articles in journals, articles published in conference proceedings, book chapters, etc.) by school. Only papers published on behalf of the university are taken into account.

10.34.2 Based on the decision of the Vice-Rector for Research, unique papers of the School of Information Technology published in the Google Scholar top 20 journals shall be added to the number of papers published in Q1 journals according to SNIP scores calculated from SCOPUS SciVal data.

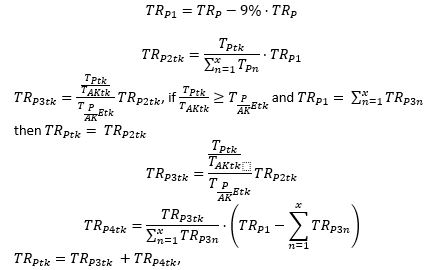

10.34.3 Funding based on a performance indicator shall be granted in two stages and the total amount for the performance indicator shall be disbursed. Prior to granting the funding, the school’s 100% target implementation rate of the performance indicator of the school is calculated based on the share of the schools Q1 papers in all Q1 papers and the amount is multiplied by the financial amount of the performance indicator.

10.34.4 The first step is to multiply the school’s 100% target implementation rate of the performance indicator by the respective annual result of the respective school. If the total financial amount of the performance indicator is not distributed in the first stage, the remaining financial amount shall be distributed proportionally to the product of the amount paid in the first stage and the undistributed amount.

10.34.5 In the case of the Estonian Maritime Academy, it is considered, by way of exception, that the share of the performance indicator is 9% until the budget for 2025 is prepared and the actual implementation rate is not taken into account.

10.34.6 The performance-based funding is obtained according to the following formula.

where the abbreviations in the formula stand for:

10.34.6.1 the total amount of performance-based funding of publications TRp;

10.34.6.2 the total amount of performance-based funding for publications minus the funding of the Estonian Maritime Academy TRp1;

10.34.6.3 the performance indicator of the school’s publications TPtk;

10.34.6.4 the number of academic staff members at the school TAKtk;

10.34.6.5 the performance-based funding based on the school’s publications TPPtk;

10.34.6.6 the school’s target for the number of papers per an academic staff member with a PhD TP/AK Etk;

10.34.6.7 the number of schools (excluding the Estonian Maritime Academy) x;

10.34.6.8 index of the concrete school (excluding the Estonian Maritime Academy) n.

10.35 The rules for calculating the performance indicator 10.23.2: the efficiency of supervision of doctoral studies:

10.35.1 The performance indicator is calculated based on the ratio of the number of PhD students listed in the study information system who defended their PhD within up to one year after the end of the nominal period of study as of 31.12 to all the number of PhD students who had to defend their doctoral degree within up to one year after the end of the nominal period of study in the corresponding year by department of the principal supervisor. The time spent on academic leave, maternity leave, parental leave and military service is deducted from the calculation of the nominal period of study. The nominal period of study is calculated based on the action plan (PhD students matriculated in the 2022/2023 academic year or later).

10.35.2 Funding based on a performance indicator shall be granted in two stages and the total amount for the performance indicator shall be disbursed. Prior to granting the funding, the school’s 100% target implementation rate of the performance indicator is calculated based on the share of the total number of students studying at the corresponding school up to one year after the end of the nominal period of study in the total number of PhD students studying at the university up to one year after the end of the nominal period of study and the result is multiplied by the financial amount of the performance indicator in the respective financial year.

10.35.3 The first step is to multiply the school’s 100% target implementation rate of the performance indicator by the respective annual result of the respective school. If the total financial amount of the performance indicator is not allocated in the first stage, the remaining financial amount shall be allocated proportionally to the product of the amount paid in the first stage and the undistributed amount.

10.35.4 In the case of the Estonian Maritime Academy, it is considered, by way of exception, that the share of the performance indicator is 9% until the budget for 2025 is prepared and the actual implementation rate is not taken into account.

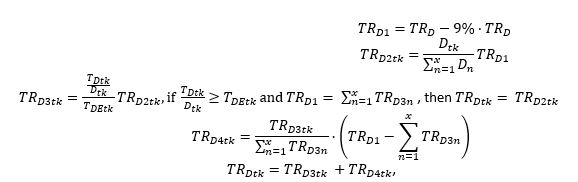

10.35.5 The funding based on the performance indicator is obtained according to the following formula.

where the abbreviations in the formula stand for:

10.35.5.1 the total amount of performance-based funding for supervision in PhD studies TRD;

10.35.5.2 the total amount of performance-based funding for supervision in PhD studies minus the funding of the Estonian Maritime Academy TRD1;

10.35.5.3 the number of PhD students at the school supposed to be graduating within NOM+1 Dtk;

10.35.5.4 the number of PhD students at the school who graduated within NOM+1 TDtk;

10.35.5.5 performance-based funding for supervision in PhD studies at the school TRDtk;

10.35.5.6 the school’s target for the share of students who graduate within NOM+1 in the total number of PhD students who graduate within NOM+1 TDEtk;

10.35.5.7 the number of schools (excluding the Estonian Maritime Academy) x;

10.35.5.8 index of the concrete school (excluding the Estonian Maritime Academy) n.

10.36 The rules for calculating the performance indicator 10.23.3: entrepreneurship:

10.36.1 First, under the performance indicator, one-off premiums are paid for spin-off companies where the university acquired a shareholding in the previous calendar year and for license agreements concluded in the previous calendar year, according to which the license fee paid to the university in the first year of validity of the license agreement is at least 5,000 euros.

10.36.2 A department is paid 10,000 euros for a license agreement and 50,000 euros for a spin-off company. If more than one department was involved in the event, the amounts will be 50% higher and their allocation among the departments will be decided by the Vice-Rector for Entrepreneurship. If a licence agreement was concluded with a university spin-off, no separate premium is paid for the license agreement. If the amount of one-off premiums exceeds 250,000 euros, the amount of all the one-off premiums shall be reduced proportionally so that the total amount of the premiums would be 250,000 euros.

10.36.3 The funding for the performance indicator not paid in one-off premiums shall be allocated between the schools proportionally to the allocation of the amount of business income in the previous calendar year.

10.36.4 Revenue from business contracts includes the revenue recognised in the report on the implementation of the university’s budget as revenue from research and development contracts and services, whereas all business income is taken into account, incl. income not deemed to be baseline funding by the state.

10.36.5 When calculating business income, a coefficient of 1.5 is applied to income received under contracts with the total value of 10,00 euros that are either:

10.36.5.1 interdisciplinary – more than one department participated in the implementation of the contract (i.e. the revenue from the contracts is divided between several departments) and/or

10.36.5.2 covered exclusively by the customer’s own funds, i.e. no public funding measures have been used.

10.36.6 The Technology Transfer Office shall keep accounts for the application of business income coefficients and the coefficients are not accumulated if both conditions are met simultaneously

10.36.7 The performance-based funding is obtained according to the following formula.

10.36.8 ![]() ,

,

where the abbreviations in the formula stand for:

10.36.8.1 performance-based funding of the school based on revenue from business contracts TRETtk;

10.36.8.2 the value of the school’s performance indicator TETtk;

10.36.8.3 the number of schools – x;

10.36.8.4 index of the concrete school n;

10.36.8.5 the total amount of performance-based funding for continuing education TRET.

10.37 Issues and disputes regarding the baseline and performance indicators related to the general education fund shall be settled by the Vice-Rector for Academic Affairs. Issues and disputes regarding the baseline and performance indicators related to the general research fund shall be settled by the Vice-Rector for Research, except for the performance indicator 10.23.3, where the disputes shall be settled by the Vice-Rector for Entrepreneurship.

11. Budget preparation

11.1 Budgets shall be prepared and drawn up in adherence to the following:

11.1.1 the university’s strategic plan, budgetary strategy, action plans and other strategic documents;

11.1.2 the structure of the university budget approved by the Finance Office, the structure of the structural unit and a financing source, schedule and other instructions provided by the Chief Financial Officer;

11.1.3 the school’s action plan;

11.1.4 the public procurement plan of the structural unit for the financial year;

11.1.5 the legislation governing the financial activities in force at the university, including the principles of calculating overheads;

11.1.6 the terms and conditions established by the sponsors;

11.1.7 sectoral reports, such as reports on teaching and learning activities and research and development, the report on the university’s partnership with society, etc., and the annual report of the previous year;

11.1.8 the revenue forecast for the coming financial year in the current budgetary strategy.

11.2 The Finance Office shall approve the deadlines and the terms and conditions (schedule) for preparing and drawing up the budget by 31 May at the latest.

11.3 In order to prepare a budget, the area directors shall submit to the Finance Office the following:

11.3.1 initial estimates in the field;

11.3.2 initial estimates of the university’s revenue in the unit’s area of activity and proposals for distribution of the estimates in sub-budgets;

11.3.3 applications for financing the offices’ and university-wide projects in their area of responsibility;

11.3.4 preliminary proposals for establishing the rates of support, etc. in their area of responsibility and concerning the university as a whole;

11.3.5 other information for drawing up a budget and its explanatory memorandum.

11.4 The Real Estate Development Director shall submit the estimation of investment property of the capital budget by investment project.

11.5 The Finance Office shall provide estimates of the loan payments and interest expenses.

11.6 The Finance Office shall provide estimates of the financial volume of the general funds and the resources allocated from the general fund to schools, the support structure, capital budget and funds. The Finance Office shall discuss the estimated allocations from the general fund with the Rector’s Office.

11.7 The Rector shall decide upon establishment of funds and their financial volume in the draft budget.

11.8 The Rector shall hold negotiations with the schools with regard to the budget, including for their financing from the general fund. Before the negotiations, the Finance Office shall provide the schools with information on the estimated revenue of the schools received in the budgets of the schools, including their structural units, as well as data on the estimated funding from the general fund.

12. Preparing, processing and approving a budget

12.1 An area director shall prepare the draft budgets of the offices and university-wide projects in his or her area of responsibility and submit the draft budgets with the accompanying explanatory memorandum to the Finance Office.

12.2 The Finance Office:

12.2.1 shall draw up a draft budget based on the draft sub-budgets of the budget;

12.2.2 shall add an explanatory note to the draft budget, taking into account the explanatory notes of the draft sub-budgets;

12.2.3 if the draft budget submitted by the area director or dean does not comply with the established conditions, the Finance Office has the right to return the draft budget and request that the deficiencies be rectified;

12.2.4 shall publish the principles of allocation of funds from the general fund of the budgets belonging to the sub-budget of the support structure in the explanatory memorandum of the budget;

12.2.5 approve the budgets in the sub-budgets of the support structure and the budgets of investment projects and repayment of principal of loans and interest costs in the capital budget after the University Board has approved the university’s budget.

12.3 A dean shall:

12.3.1 distribute the allocations from the general funds between the departments and the dean’s office;

12.3.2 together with the heads of structural units, set objectives of the structural units of the school for raising revenue;

12.3.3 prepare the draft budget of the school, including the dean’s office and the explanatory memorandum, approve the department’s draft budget and submit these to the Finance Office;

12.3.4 prepare a budget strategy forecast for the school’s revenue;

12.3.5 discuss the school’s draft budget in the school council;

12.3.6 publish the principles of allocation of funds from the general fund of the budgets of the departments in the explanatory memorandum of the budget;

12.3.7 approve the budgets of the Dean’s Office and departments after the University Board has approved the university’s budget;

12.3.8 discuss implementation of the school budget in the school council.

12.4 The head of the department shall:

12.4.1 approve the budgets of the financing sources of the department;

12.4.2 prepare the department’s draft budget, discuss it in the department council and submit it to the dean;

12.4.3 decide on budgetary matters of the structural unit, including issues regarding self-financing of the department’s projects, covering the deficits in the financing sources, using the surplus and other similar issues;

12.4.4 discuss implementation of the department’s budget in the department council.

12.5 The Rector shall submit a draft budget to the Senate no later than by the last Senate session of a calendar year held in December.

12.6 The Senate shall submit the budget to the University Board for approval.

12.7 The budget approved by the University Board will be published on the university’s website.

12.8 If the university’s budget is not approved by the beginning of the financial year, the Rector shall, in agreement with the University Board, establish a temporary procedure for covering expenses.

13. Making amendments and adjustments in the budget

13.1 The university’s budget will be amended if a significant deviation from the approved budget revenue, expenses, investment transactions, financing operations or cash flows occurs or is expected.

13.2 A budget is amended according to the same procedure as the one applied upon processing and approving a budget.

13.3 In the case of minor deviations from the approved budget, a dean, a head of a department or an area director has the right to make amendments and adjustments in the budget of the department or office respectively and in university-wide projects throughout the financial year provided that:

13.3.1 the estimated revenue will not decrease compared to the amount of revenue in the approved budget;

13.3.2 the overhead allocation into the general fund will not be smaller than the one in the approved budget;

13.3.3 the budget complies with the terms and conditions set out in clause 14.8.

13.3.4 the amount in each budget line and the total amount of the budget of the school or structural unit remains the same.

13.4 A head of a department and an authorising officer have the right to cover expenses that are bigger than set out in the approved budget if the dean has approved the relevant budget adjustments and provided that, following the change, the budget of the school remains in balance.

13.5 The Real Estate Development Director has the right to make adjustments in the capital budget:

13.5.1 by increasing funding of an investment project if an additional targeted support is allocated for that;

13.5.2 if the Rector decides to allocate additional funding for an investment project, initiate new investment projects from university funds or other financing sources.

13.6 The Rector has the right to decide, without amending the budget, on funding the investment projects specified in clause 13.5.2. or on increasing it by up to 300,000 euros compared to the approved budget.

13.7 The Finance Office processes the proposed budget amendments twice a year, during the preparation of the semi-annual and annual reports.

13.8 Budget adjustments come into force if they meet the requirements set out in the Regulations and after they have been approved by the Finance Office.

14. Rights and obligations upon implementation of the budget

14.1 The Finance Office shall monitor implementation of the school, support structure, fund and capital budgets.

14.2 The dean and the head of the department shall monitor implementation of the department budget. The dean shall monitor implementation of the budget of the dean’s office.

14.3 The head of a structural unit and the authorising officer shall monitor implementation of the budget of a financing source.

14.4 The Finance Office has the right to give orders for appropriate implementation of the budget and to check receipt of funds and that the funds are used for their intended purpose and in compliance with the goals of the university.

14.5 The head of a structural unit has an obligation and responsibility to consistently monitor adherence to the budget of the structural unit and its financing sources, the right to receive information needed for that from the heads of other structural units, the authorising officers and the Finance Office and to immediately inform the Finance Office of any deficiencies.

14.6 The Finance Office shall keep accounts on the implementation of the budget and make sure that the corresponding information is communicated in a report on the intranet. Information on the implementation of the budgets of all structural units and financing sources, the related revenue, expenses, investment transactions, financing operations and additional information on cash flows is published regularly on the intranet.

14.7 If the actual revenue of a structural unit in a financial year exceeds the revenue in the adopted budget, the head of the unit has the right to decide how to spend the funds.

14.8 If the actual revenue of a structural unit in a financial year is lower than in the adopted budget and the deficit exceeds the positive aggregate result, the head of the structural unit is obliged to reduce the expenses by the same amount, i.e. so that the aggregate result would not remain negative. If a budget that has a negative outturn is approved, the negative outturn must not increase.

14.9 In case the overrun on expenditure of a financing source, budget or cash is greater than budgeted (unapproved expenditure overruns) or the expenditure exceeds the budgeted amount of expenditure and the revenue does not increase in the same amount,

14.9.1 the head of the structural unit shall inform the dean or area director and the Chief Financial Officer thereof;

14.9.2 the head of the structural unit shall analyse the financial situation and decide on the measures to be taken to resolve the situation and obtain approval therefor from the dean or area director and notify the Finance Office of the measures in writing;

14.9.3 the Finance Office has the right to suspend expenditures from the budget or financing source of a structural unit until a solution is provided for elimination of expenditure overruns;

14.9.4 the expenditure must not be suspended if the expenses shall be incurred arising from law or a contract and the suspension thereof may result in financial loss to the university;

14.9.5 The Rector may appoint a fund manager to a structural unit.

14.10 In the case of possible expenditure overruns of an investment project in the capital budget, the Real Estate Development Director has the right to allow it to the extent that another investment project in the capital budget has adequate surplus of funds to cover the overruns.

14.11 If the funds provided in the capital budget are not sufficient to service a loan, the Finance Office shall notify the Rector of the situation and develop measures for resolving the situation.

14.12 Expenditure overruns are permitted in budgets (a credit limit is opened) and approval thereof is carried out as follows:

14.12.1 overrun on expenditure in the budget of a financing source is permitted if this has been agreed upon in a contract entered into with the sponsor and/or the there is no budget overrun of the structural unit and the head of the structural unit has given the corresponding consent;

14.12.2 overrun on expenditure in the budget of a structural unit (incl. the dean’s office) of a school is permitted if there is no budget overrun of the school and the dean has given the corresponding consent;

14.12.3 short-term overrun on expenditure in the budget of a school is permitted with the consent of the Chief Financial Officer. The Chief Financial Officer shall inform the Rector of the expenditure overruns of a school;

14.12.4 short-term overrun on expenditure in the project budget of a school, structural unit or the university is permitted in the case of investment activities;

14.12.5 short-term overrun on expenditure in the budget of a department or university-wide project is permitted with the consent of the area director and the Finance Office.

14.13 Expenditure overruns shall be covered from the budget of the structural unit, who is responsible for carrying out the activity that caused the expenditure overruns and in whose budget the expenses, investment transactions, financing operations and cash outflows that caused the expenditure overruns are recognised.

14.14 In order to avoid expenditure overruns of a structural unit or financing source, the head of the structural unit can apply for internal loan to cover long-term expenditure overruns as follows:

14.14.1 the Finance Office has the right to grant internal loan within the limit established by the University Board at the expense of the university’s cash flows;

14.14.2 before granting an internal loan, the Finance Office shall assess the financial sustainability of the structural unit that applied for the loan;

14.12.3 the loan granted shall be recorded by written agreement and carried out as an internal settlement between financing sources;

14.12.4 an agreed interest rate may be applied to an internal loan, the revenue from which is treated as an allocation to the general fund.

14.15 The budget of university-wide activities, incl. funds, can only be used for their intended purpose and in compliance with the budget.

14.16 The cash balance created upon implementation of the budget of a financial year is carried forward to the next financial year accounts as follows:

14.16.1 the cash balance of an academic structural unit or a financing source of a target-financed project as at the end of the financial year is carried forward into the next financial year, as a rule into the same financing source, where the balance was created;

14.16.2 if the cash balance of a financing source is created from project grants or targeted allocations, the cash balance is maintained until the activities have been carried out, for which the support was granted.

14.17 If the amount of general funds at the end of a financial year is smaller than estimated due to a shortfall in receipts of overhead allocations, the Rector shall decide on the proposal of the Finance Office how the budget will be balanced.

14.18 If the amount of general funds at the end of a financial year is greater than estimated due to budget over-performance, the cash balance created will be used to cover the expenditure of the general funds in the following periods or, based on the Rector’s decision, to cover the expenditure in the university’s budget.

14.19 If the amount of activity support and baseline funding received in the general funds is greater than the budgeted amount and it is not necessary to cover the previous shortfall of the general funds, the excess amount shall be distributed by the Rector’s decision.

15. Budget implementation report

15.1 A budget implementation report shall be drawn up annually and semi-annually.

15.2 An accrual basis budget implementation report shall correspond to an accrual basis accounting report.

15.3 A budget report shall be based on the chart of accounts. The compliance of budget lines and the chart of accounts shall be approved by the Finance Office.

15.4 The heads of structural units and the authorising officers must make sure that the source documents of accounting are submitted and approved no later than by 15th day of the month following each month.

15.5 A report on implementation of an annual budget shall be prepared on the university as a whole, as well as on all the structural units (on the budget form established for structural units) no later than by 31 March.

15.6 A report on implementation of an annual budget shall be processed and approved by the management bodies of the university in compliance with the Tallinn University of Technology Act. Additional reports shall be submitted to the management bodies upon request.

15.7 Information on the implementation of the quarterly budgets of the university, sub-budgets and budgets of structural units shall be made available to the deans and heads of structural units on the intranet by the last day of the month following the quarter.

16. Liability of the head of the structural unit and the fund manager

16.1 The head of a structural unit shall be responsible for proper implementation of the budget of the structural unit.

16.2 The authorising officer shall be responsible for proper implementation of the budget of the financing source.

16.3 Improper budget implementation means a following situation:

16.3.1 the actual expenditure exceeds the budgeted expenditure and there is no additional revenue to cover the expenditure, which thus result in expenditure overruns;

16.3.2 there are expenditure overruns that have not been agreed in the budget or that exceed the agreed expenditure overruns;

16.3.3 ineligible expenditure unrelated to the university is incurred;

16.3.4 other situations that cause cash deficit to the university.

16.4 In case shortcomings occur in the implementation of the budget by the head of a structural unit or authorising officer, the Rector has the right, depending on the nature of the shortcoming, the explanations provided by the head of the structural unit and proposal made by the Finance Office:

16.4.1 to suspend the expenditures and reclaim the expenses incurred;

16.4.2 suspend new commitments;

16.4.3 to make a warning to the person responsible in accordance with the Employment Contracts Act, in the case of repeated warning cancel the employment contract in full or in part or reduce wages;

16.4.4 to claim compensation of the loss from the person responsible, including compensation of direct loss and loss of revenue;

16.4.5 to refuse to make payments to the person responsible until the damage caused by him or her has been compensated;

16.4.6 to resort to other legal remedies with regard to the person responsible;

16.4.7 to appoint a fund manager to the structural unit.

16.5 If a fund manager has been appointed to a structural unit, no payments are made from financing sources of the structural unit without the approval of the fund manager.

16.16 To balance the budget of a structural unit, the fund manager shall apply at least the following measures:

16.16.1 the salaries of the employees of the structural unit are not increased, no additional remuneration and bonuses are paid to them, unless provided otherwise by legislation or valid contracts;

16.16.2 no new employees are recruited to the structural unit, except in cases where recruitment is inevitable for generating revenue and for fulfilment of the obligations of the university.

16.17 If the fund manager fails to balance the budget of the structural unit within the specified period, the fund manager shall provide the Rector an overview of the situation and the Rector shall decide on further measures.

17. Classification and opening of financing sources

17.1 The Finance Office opens financing sources in the business software for a fixed or indefinite period.

17.2 As a rule, the main activity of a structural unit is recognised in permanent financing sources as follows:

17.2.1 a structural unit has one financing source where permanent main activities are recorded;

17.2.2 a financing source is opened in accordance with the legal act under which the structural unit is established;

17.2.3 the financing source will stay open until the related structural unit exists.

17.3 Other permanent financing sources are opened on a reasoned proposal of the structural unit and based on the decision of the Finance Office.

17.4 The activities carried out during a specific period and for a specific purpose are recognised in fixed-term financing sources.

17.5 A fixed-term financing source is opened in case of a specific financing decision or availability of funding as follows:

17.5.1 in order to recognise projects and research funding and other similar funding, a financing source is opened in the document management system on the basis of a document confirming such funding;

17.5.2 in order to recognise the funding of business contracts, a financing source is opened in the document management system after the contract is concluded;

17.5.3 in order to recognise the funding of a project grant, a financing source is opened in the document management system;

17.5.4 a financing source for continuing education is opened with the approval of the Head of Open University;

17.5.5 for financing from the funds, a financing source is opened by the Finance Office based on the order of the person in charge;

17.5.6 in other cases, a fixed-term financing source is opened on the basis of the decision of the Finance Office. The corresponding reasoned proposal may be made by the head of the structural unit.

18. Effectiveness and purposefulness of costs, obligations and liability

18.1 The head of a structural unit is responsible for the effectiveness and purposefulness of the costs incurred from the financing sources in the budget of the structural unit, the expenditure overruns and for fulfilling the obligations arising therefrom.

18.2 The authorising officer is responsible for the effectiveness and purposefulness of the costs incurred from the financing source, the expenditure overruns and for fulfilling the obligations arising therefrom.

18.3 If the term of a fixed-term financing source expires and the financial operations have been executed, the head of the structural unit and the authorising officer are obliged to close the financing source during the financial year, whereas:

18.3.1 in the case of expenditure overruns of a financing source, the authorising officer shall find financial resources to cover the overruns;

18.3.2 in the case of surplus of a financing source, the authorising officer shall, with the approval of the head of the structural unit, make a proposal to the Finance Office for further use of the surplus;

18.3.3 if the deadline of a financing source expires and no request has been submitted to the Finance Office for extension of the deadline and the financing source has not been closed, the Finance Office has the right to close the financing source and direct the corresponding expenditure overruns or surplus into the budget of the structural unit, as a rule, into the financing source where main activities are recognised.

18.4 Financial lease/lease intents must be approved by the Chief Financial Officer in advance.

18.5 The obligations and liability of the authorising officer of a financing source:

18.5.1. is obliged to use the university’s resources in compliance with legislation, for the intended purpose and rationally and avoid overruns;

18.5.2 is obliged to monitor compliance with the budget he/she is in charge of and to inform immediately his/her direct superior or head of the department of any deficiencies in accordance with the Financial Regulations;

18.5.3 is obliged to monitor implementation of the budget, to inform the Finance Office of the changes regarding the financing sources included in the budget, e.g. the extension of the term of the financing source, changes regarding the authorising officer or approver of the financing source;

18.5.4 is obliged to adhere to the procedures established by the university and the Public Procurement Act and avoid any conflict of interest upon implementation of the budget;

18.5.5 is responsible for ensuring that the quantities, prices and other terms recorded in the document correspond to the previously concluded contracts;

18.5.6 is responsible for ensuring that the transaction is legal and expedient and in line with the budget;

18.5.7 is responsible for the implementation and the balance of the budget and the balance of cash flow.

19. Other terms and conditions regarding financing source expenditure, self-financing and reporting

19.1 Remuneration for annual leave, including state taxes, are recognised in the financing source, where the wages that are the basis for calculating remuneration for annual leave, are recognised. If a financing source has been closed by the time of calculation of remuneration for annual leave or remuneration for annual leave cannot be paid from the financing source, the remuneration for annual leave is recognised in the permanent financing source (of the main activity) of the structural unit, where the employee is employed at the moment when the need to calculate remuneration for annual leave arises or in the financing source indicated by the head of the structural unit.

19.2 Self-financing and refunds of VAT shall be recognised in the financing source related to the grant by financial year.

19.3 In the case of financing sources, where grants are recognised, the reports submitted to the sponsor must be approved by the Finance Office. A report shall be submitted to the Finance Office for approval no later than five working days before submission of the report to the sponsor.

20. Classification of service providers and services

20.1 The types of services provided by the structural units of the university are degree level education services, knowledge-based services and administrative services.

20.2 Degree level education service means the service provided to the students of Tallinn University of Technology based on a degree level programme, where the recipient of the service covers the cost of tuition to the extent determined by the university.

20.3 Knowledge-based services include:

20.3.1 training services, incl. in-service training and retraining, other training or courses, workshops, etc.;

20.3.2 R&D services, incl. research, development, consultancy, laboratory, conference and other R&D services.

20.4 Administrative services include technical, transport, library, museum, document management and other services and rental of university premises.

21. Principles of pricing of services, excluding internal services

21.1 The prices of standard services are set out in the price calculation or price list.

21.2 The price of a service shall be based on the full cost of the service, based on which the total price is obtained, i.e. the price that covers the full cost of the service (actual direct and indirect costs) and the operating margin (markup added onto the service price obtained based on full cost). VAT is added to the total price of a service in cases provided by law.

21.3 The final price of a service determined by a price calculation is set by the service provider, who may, in exceptional cases, set a price lower than the total price if the service price obtained is significantly higher than the market price and is thus not competitive. A price calculation shall be approved by the head of the structural unit.

21.4 The price of a service established by a price list shall be approved by the Senate, area director or head of the structural unit as follows:

21.4.1 the tuition fee rates for students and external students shall be established by the Senate;

21.4.2 the tuition fee for continuing education course participants and other price lists concerning the university as a whole shall be approved by the area director in whose area of activity the service belongs;

21.4.3 the price lists of the services of a structural unit shall be approved by the head of the structural unit.

21.4.4 A structural unit responsible for providing a standard service shall submit an explanation of pricing together with the draft price list.

22. Cost accounting upon pricing of services

22.1 Direct costs of a service are directly related to the provision of a service or performance of a contract and include the following:

22.1.1 gross remuneration of the employees providing the service and the applicable taxes and payments established by law;

22.1.2 other costs related to the provision of the service (incl. costs of materials, travel, transport, etc. and depreciation of equipment).

22.2 The indirect costs of a service are the university’s overheads accompanying provision of the service or performance of the contract that cannot be regarded as direct costs since they are not directly related to the activity or it is not rational to classify them as direct costs for some reason. The indirect costs of a service include the following:

22.2.1 management, legal, marketing and communications and document management services;

22.2.2 the service of organisation of studies;

22.2.3 the service of organisation of research;

22.2.4 the service of organisation of research activities;

22.2.5 personnel services;

22.2.6 information technology service;

22.2.7 accounting, financial management and procurement administration services;

22.2.8 other support services, incl. library services;

22.2.9 real estate management service, incl. expenses of the premises, depreciation of buildings.

22.3 The service price is calculated using the following formula:

![]() TH – service price

TH – service price

22.3.1 OK– direct costs

22.3.2 ![]() – university overhead fee rate

– university overhead fee rate

22.3.3 KKp – percentage of additional indirect costs

23. Supervision over pricing of services

23.1 Supervision over compliance of pricing of a service with the requirements shall be exercised in accordance with the university’s legislation.